Menu

Contributed by Idea Collective Member:

Bookkeeper, Advisor, Money Coach

This is a great place to start for any small business but even the best can fail if they don’t carefully manage their money from the very beginning.

Most business owners are familiar with the Profit and Loss Statement (also called an Income Statement) – and they should be – but it’s just a small part of the financial picture and leaves out other ways that money flows in and out of your business.

An Income statement measures your sales, expenses, and earnings for the period: Revenue minus Expenses = Net Income. It does not measure the cash that flows in and out of the company bank accounts.

Here are a few examples of what is not measured:

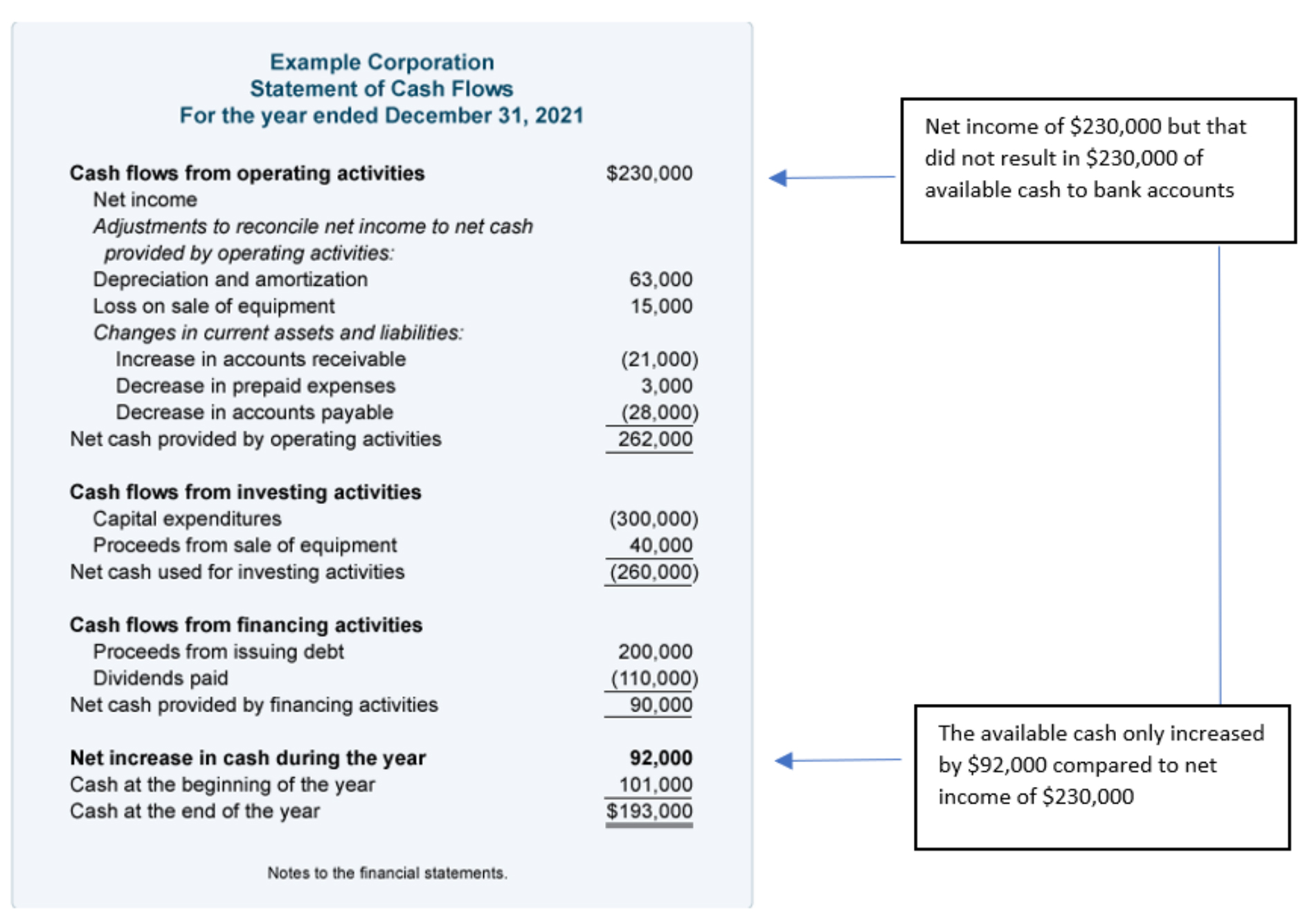

As you can see from the example below, positive net income does not equal money in the bank.

A business owner was rocking their sales (200K+) and paying themselves from the business. They were turned down for a personal home loan because their records did not provide an accurate picture of the business finances. The owner was a bit confused because “they made good money last year” but decided to contract bookkeeping services to clean things up so they could get a loan and buy their new home.

Books are up-to-date and in ship-shape condition, yay!

Now for the bad news, they may have been rocking their sales BUT:

They now get the news that if they don’t right the ship quickly – they’ll be out of business soon. Yikes!

In this scenario, the records were just a small part of the problem. Cash was flowing in and out of the business in many ways and the owner had no visibility to it. That’s where the Statement of Cash Flows comes in.

A business owners understanding of cash inflows and outflows is critical for making good business decisions and for meeting their obligations to employees, suppliers, and lenders – short-term and long-term. It’s used to make sure a company has enough cash to meet its day-to-day expenses and to project cash flows in the future. The Statement of Cash Flows provides this information.

For Example: It measures cash flowing in and out from:

Becoming familiar with the ways cash flows in and out of your business could mean the difference between failure and success so taking the time to review and understand your Statement of Cash Flows is important. It looks confusing at first but in a short period of time, you’ll master this information and be able to quickly understand the full picture of what is happening with your money.

Check out this article from Investopedia for some more in-depth information.

Spreadsheet: Here is a downloadable template from SCORE that is a great starting point. You can track actual results by month and input your projected numbers to gauge how long your cash will last.

Quickbooks: How to run a Statement of Cash Flows

Small steps lead to big changes so take a step toward mastering your money and improve your chances of success TODAY. Schedule time on your calendar to review the information, set up the tools, or contact your bookkeeper so you can be a rockstar with your money as well as your business.

If you need help along the way, the Idea Collective community is there to help.

© Small Step Solutions, LLC 2024 | Web by KP Design